How to Avoid Probate in Illinois: A DuPage County Guide

Most people who ask how to avoid probate in Illinois have heard the horror stories: the year-long court case, the legal fees, the family home tied up while everyone waits on a judge. Avoiding probate is very doable here with the right tools, most simple to set up while you are healthy. But start with the most common misunderstanding: a will does not avoid probate. It actually sends your estate into probate; it just tells the court what you wanted once you get there.

Our firm has handled estate planning and probate for DuPage County families since 1990, so we have watched the same avoidable problems repeat for a generation. This guide covers the tools that keep assets out of court, the small estate affidavit and its dollar limit, and the funding step that quietly sinks more plans than anything else. Where a statute controls, we cite it so you can check it yourself.

TL;DR: A will does not avoid probate in Illinois; it actually directs the estate through the probate court. The tools that keep assets out of court are a funded revocable living trust, joint tenancy or tenancy by the entirety, payable-on-death and transfer-on-death account designations, a Transfer on Death Instrument for a home, and, for a modest estate, the small estate affidavit. Under 755 ILCS 5/25-1, an estate with no real estate and personal property of $150,000 or less can be settled with a small estate affidavit and no probate case at all. The single biggest failure point is an unfunded trust: a trust only avoids probate for the assets you actually retitle into it.

Why avoiding probate matters in Illinois

Probate is the court-supervised process of proving a will (or, if there is none, following the state's intestate administration rules), paying debts and taxes, and transferring what is left to the heirs. Three things make it worth avoiding:

- Cost. Court fees, publication, bond in some cases, and attorney time all come out of the estate. We break the numbers down in how much probate costs in Illinois.

- Time. Illinois builds in a mandatory waiting period for creditors (more below), so even a simple, uncontested estate rarely closes quickly.

- Privacy. Probate is public: the will, the inventory of assets, and the names of the heirs become part of the record anyone can request.

Probate is not always a disaster, and a good estate planning attorney will tell you when it is the right path. But to keep your family out of court, planning ahead is almost always cheaper and faster than probate after the fact.

What probate actually costs and takes in DuPage County

A DuPage County estate is administered through the 18th Judicial Circuit at the DuPage County Judicial Center, 505 N. County Farm Road, in Wheaton, where the Circuit Clerk's Probate Division handles the filings through Illinois's mandatory e-filing system. The creditor claim period drives the timeline more than anything else: once an estate is opened, Illinois requires notice to creditors, published (once a week for three successive weeks) and mailed to known creditors. Under 755 ILCS 5/18-3, a claim is barred if it is not filed by the later of six months from the date of first publication or three months from the date notice is mailed or delivered to a known creditor. So six months from first publication is the floor, a known creditor's deadline can fall later, and even a clean estate cannot skip this waiting period. See how long does probate take in Illinois.

The assets that avoid probate are the ones that never enter the courthouse.

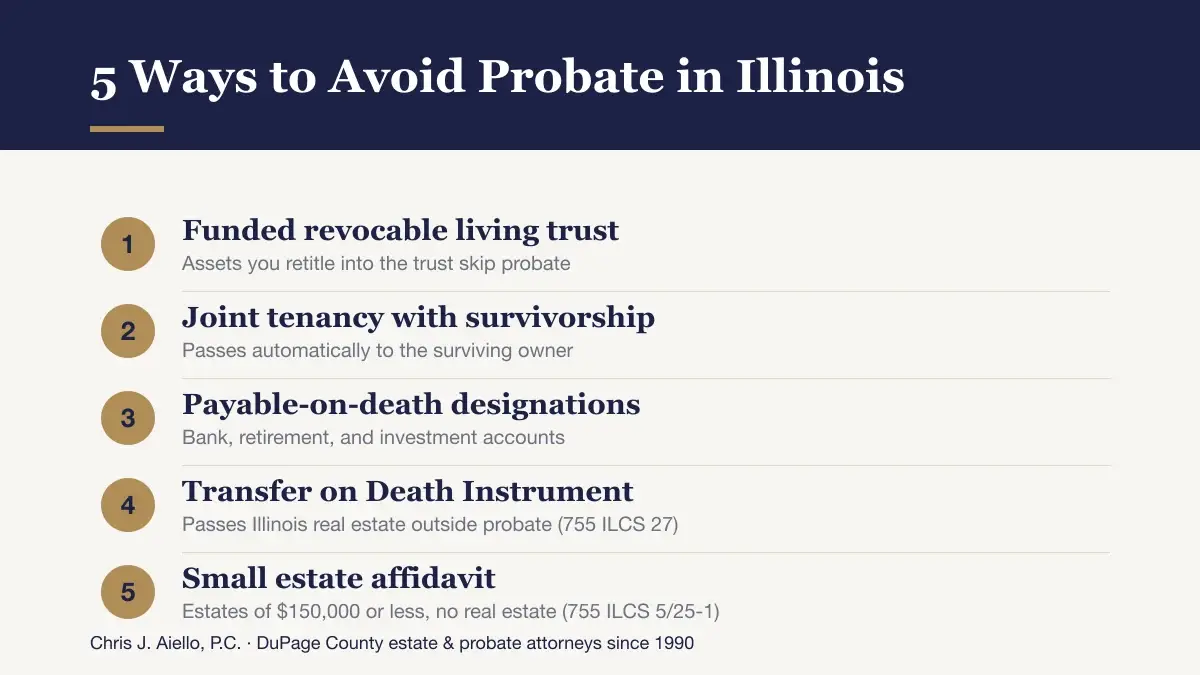

The main tools to avoid probate in Illinois

Avoiding probate is about matching the right tool to each asset. Here are the five that do the heavy lifting.

1. A revocable living trust

A revocable living trust is the most complete probate-avoidance tool for most families. You move your assets into it and control them as trustee; at death the successor trustee distributes everything privately, and it also lets someone manage your assets if you become incapacitated (which a will cannot do). The catch: it only works for assets you retitle into it, so an unfunded trust avoids nothing (the number-one failure point, below).

2. Joint tenancy and tenancy by the entirety

Property in joint tenancy with right of survivorship passes automatically to the surviving owner, outside probate; married couples can use tenancy by the entirety for a primary residence, which adds creditor protection. But it only postpones the problem: when the last owner dies the asset still needs a plan. Adding a non-spouse joint owner (say, a child) can also trigger gift-tax issues, expose the asset to that child's creditors or divorce, and disinherit your other children.

3. Payable-on-death and transfer-on-death designations

Bank accounts can carry a payable-on-death (POD) designation, brokerage and investment accounts a transfer-on-death (TOD) designation, and retirement accounts and life insurance already pass by beneficiary designation. On death the asset goes straight to the named beneficiary, outside probate, and these cost little or nothing to set up. The caveat: they are only as good as the paperwork, and a stale, missing, or poorly chosen beneficiary is a common way an asset falls back into probate.

4. Transfer on Death Instrument for real estate

Illinois lets a real estate owner name a beneficiary who receives the property automatically at death, using a Transfer on Death Instrument (TODI) under the Real Property Transfer on Death Instrument Act, 755 ILCS 27/. You keep full ownership and control during life, can revoke it, and the property passes outside probate without the cost of a full trust. Since January 1, 2022 (Public Act 102-068), a TODI can transfer any Illinois real estate, residential or commercial. It must be properly drafted, witnessed, and recorded with the DuPage County Recorder before death, and it does not help with incapacity the way a trust does.

5. The small estate affidavit

For smaller estates with no real estate, Illinois offers an affidavit that lets heirs collect assets without opening a probate case at all. Because its dollar limit is specific and was recently raised, it gets its own section next.

The $150,000 rule: Illinois small estate affidavit, precisely

Under 755 ILCS 5/25-1, an heir can use a small estate affidavit to collect a decedent's assets without a full probate case when two conditions are met:

1. The estate's personal property does not exceed $150,000 (excluding motor vehicles registered with the Illinois Secretary of State, which transfer separately), and 2. There is no real estate in the estate that has to pass through probate.

The $150,000 threshold is current: Public Act 104-346 raised it effective August 15, 2025, for deaths on or after that date. For a death before then the older, lower limit applies, so the date of death controls.

The oath matters. The affiant swears to who died, what the assets are, who the heirs are, and that debts and taxes will be handled in the order Illinois law requires, and is personally liable for distributing the assets improperly, such as paying the wrong people or ignoring a valid creditor.

The other hard limit is that any probate real estate defeats the affidavit. A house in the decedent's own name with no TOD instrument, joint owner, or trust puts the affidavit off the table and forces probate, which is why pairing a TOD instrument or trust with your home matters so much. When the estate qualifies, it settles in days, not the months a probate case takes.

Funding the trust is the step everyone skips

If you take one thing from this guide, take this: an unfunded trust does not avoid probate. We have seen well-drafted trusts sit in a drawer while the owner kept their house and accounts in their own name; at death, everything outside the trust went straight to DuPage probate, the exact outcome the trust was meant to prevent.

Funding means retitling your assets into the trust's name, in three moves:

- Real estate: moved into the trust by a new deed recorded with the DuPage County Recorder. Until that deed is recorded, the house is not in the trust.

- Financial accounts: bank, brokerage, and investment accounts retitled to the trust, or given matching POD/TOD designations.

- Beneficiary designations: retirement accounts and life insurance coordinated with the plan, so a designation does not accidentally override the trust.

Funding is not a one-time chore: every new property, account, or bank change needs to come into the plan, which is why a trust fully funded in 2015 can be full of holes by 2026.

Beneficiary designations gone wrong

POD, TOD, retirement, and life insurance designations bypass the will and the court, which is what makes them dangerous when wrong. Three mistakes pull an asset right back into probate:

- Naming a minor child directly. A minor cannot legally receive a large inheritance, so a court may appoint a guardian of the estate until age 18 (the court involvement you were avoiding). A trust for the child is better.

- Naming an ex-spouse. People update the will and forget the 401(k). The form controls, not your intentions, so a stale designation can pay out to a former spouse.

- Naming "my estate." This voluntarily routes the asset into probate, a self-inflicted problem avoidable by naming actual people or a trust.

The fix: review these when you build your plan and after every major life event, and coordinate them with your wills and trust.

Spouse's and child's awards, and the Illinois estate tax

Spouse's and child's awards. Illinois law protects a surviving spouse and dependent children regardless of your plan. It provides a spouse's award, a statutory amount set aside for the surviving spouse's support (not less than $20,000, plus not less than $10,000 for each minor child), under 755 ILCS 5/15-1. When there is no surviving spouse, a separate child's award applies under 755 ILCS 5/15-2. These awards can have priority over other claims and even some gifts in a will, one more reason to plan with an attorney who knows how the pieces interact.

Avoiding probate is not the same as avoiding estate tax. Illinois imposes its own estate tax, separate from the federal estate tax, and keeping assets out of probate does nothing to reduce it: probate is a court process, while the estate tax is a tax on the value of what you leave. The exclusion amount and rates can change, so confirm the current figure for the year of death. If your estate is large enough to face it, you need a plan built for tax as well as transfer.

A DuPage decision table: which tool for which situation

The right tool usually maps cleanly to the asset. Here is how we think about it for DuPage families:

| Asset or situation | Best probate-avoidance tool | Watch out for |

|---|---|---|

| House or condo (single owner) | Transfer on Death Instrument (755 ILCS 27/) or a funded living trust | Deed must be recorded with the DuPage County Recorder before death; a house left in your name alone forces probate |

| House owned by a married couple | Tenancy by the entirety, then a trust or TODI for the second death | Survivorship only solves the first death; plan for the last owner |

| Bank / checking / savings | POD designation | Keep the named person current; avoid naming a minor |

| Brokerage / investment account | TOD designation | Coordinate with the overall plan so it does not conflict |

| Retirement account / life insurance | Named beneficiary (person or trust) | Never name "my estate"; update after divorce or a death |

| Small cash estate, no real estate | Small estate affidavit (755 ILCS 5/25-1), personal property up to $150,000 | Affiant is personally liable; any probate real estate defeats it |

| Car titled in Illinois | Secretary of State small estate / TOD process | Excluded from the $150,000 personal-property count |

| Minor children involved | Living trust naming a trustee for the children | Never leave assets outright to a minor; name a guardian in your will |

| Blended family or complex goals | Living trust with tailored instructions | This is where DIY forms fail most often |

Use this as a starting map, not a substitute for advice. The interactions between these tools (and the Illinois estate tax) are where a conversation with an estate planning attorney earns its keep.

Talk to a DuPage County attorney

Avoiding probate in Illinois is not about one clever document. It is about matching the right tool to each asset, funding what needs funding, keeping beneficiary designations current, and knowing where the Illinois estate tax and the spouse's and child's awards still apply. Our firm has helped DuPage County families do exactly that since 1990, and we would rather set up a plan that works than watch a family sort it out in the Wheaton courthouse later.

If you want a clear read on which tools fit your situation, the first consultation is free. Call (630) 833-1122.

External authority cites to embed (neutral only): Illinois Probate Act, 755 ILCS 5 (including 25-1, 15-1, 15-2, 18-3) and the Real Property Transfer on Death Instrument Act, 755 ILCS 27/, at ilga.gov; Public Act 104-346 at ilga.gov; small estate and probate basics at illinoislegalaid.org; DuPage County Circuit Court Clerk (Probate Division) and DuPage County Recorder at the county's .gov site; estate planning basics via ISBA public guides.